Mercurius.

Mercurius.

I built it to win. Then I did the harder thing — I built it to tell me the truth.

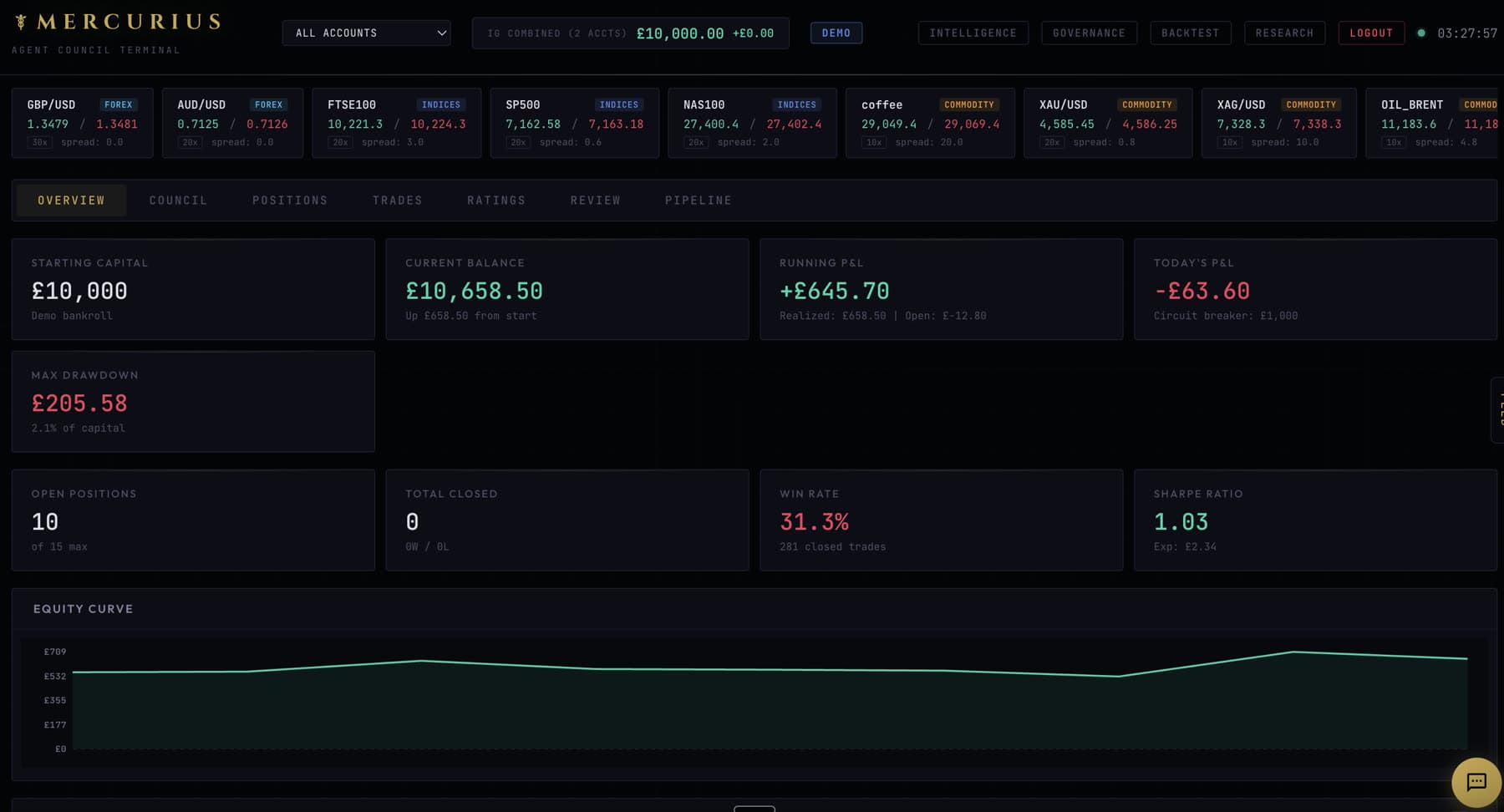

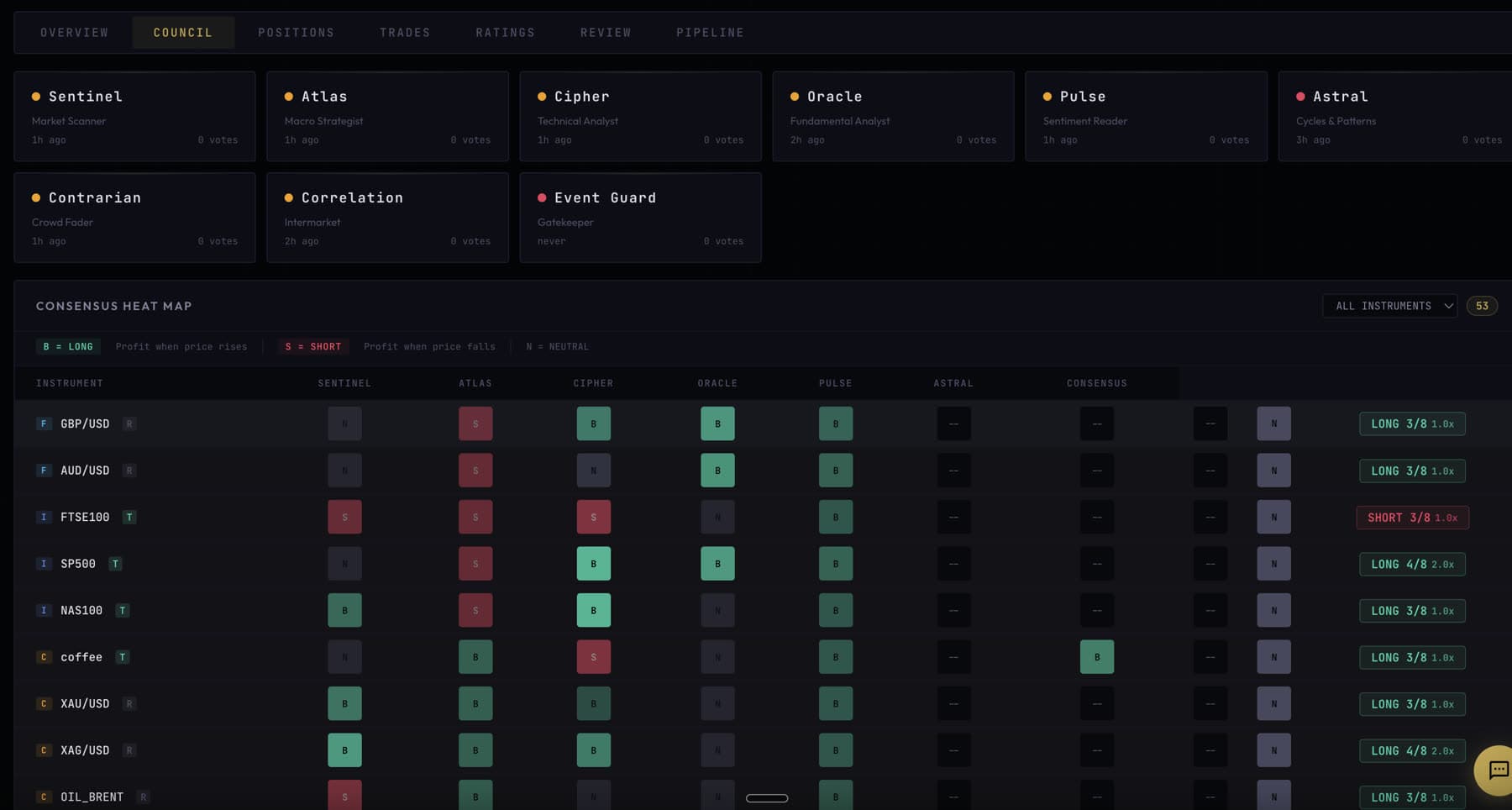

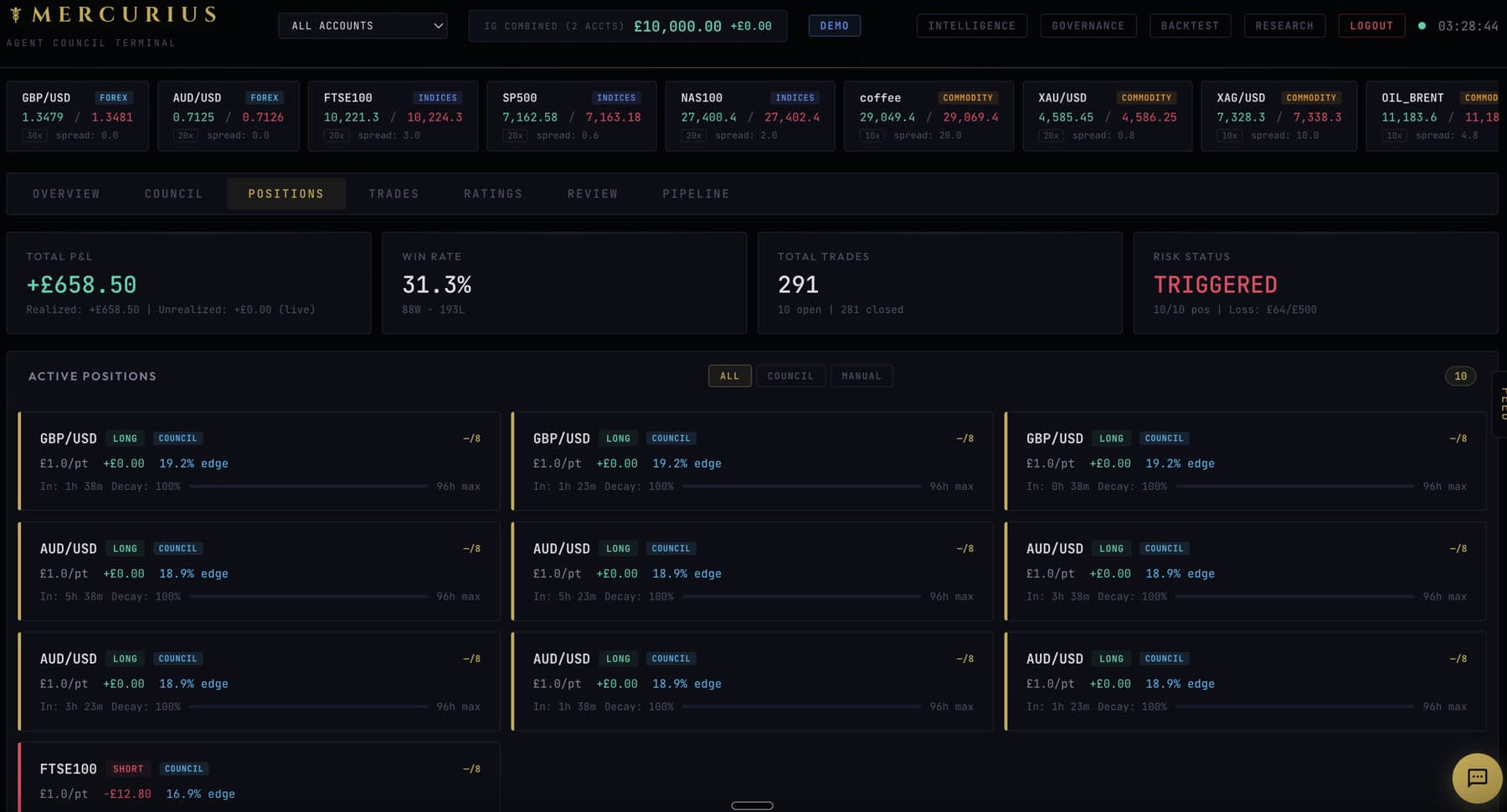

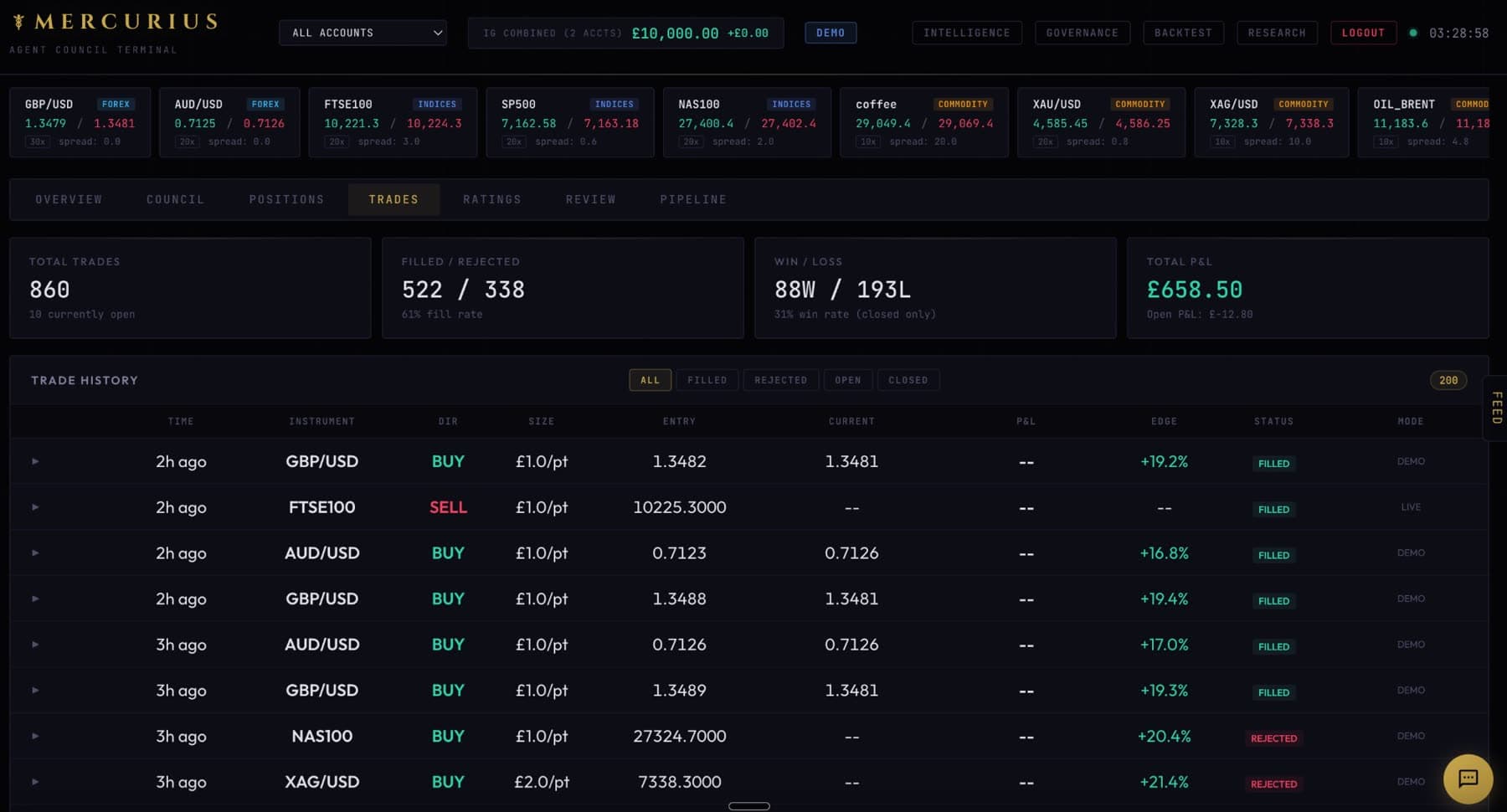

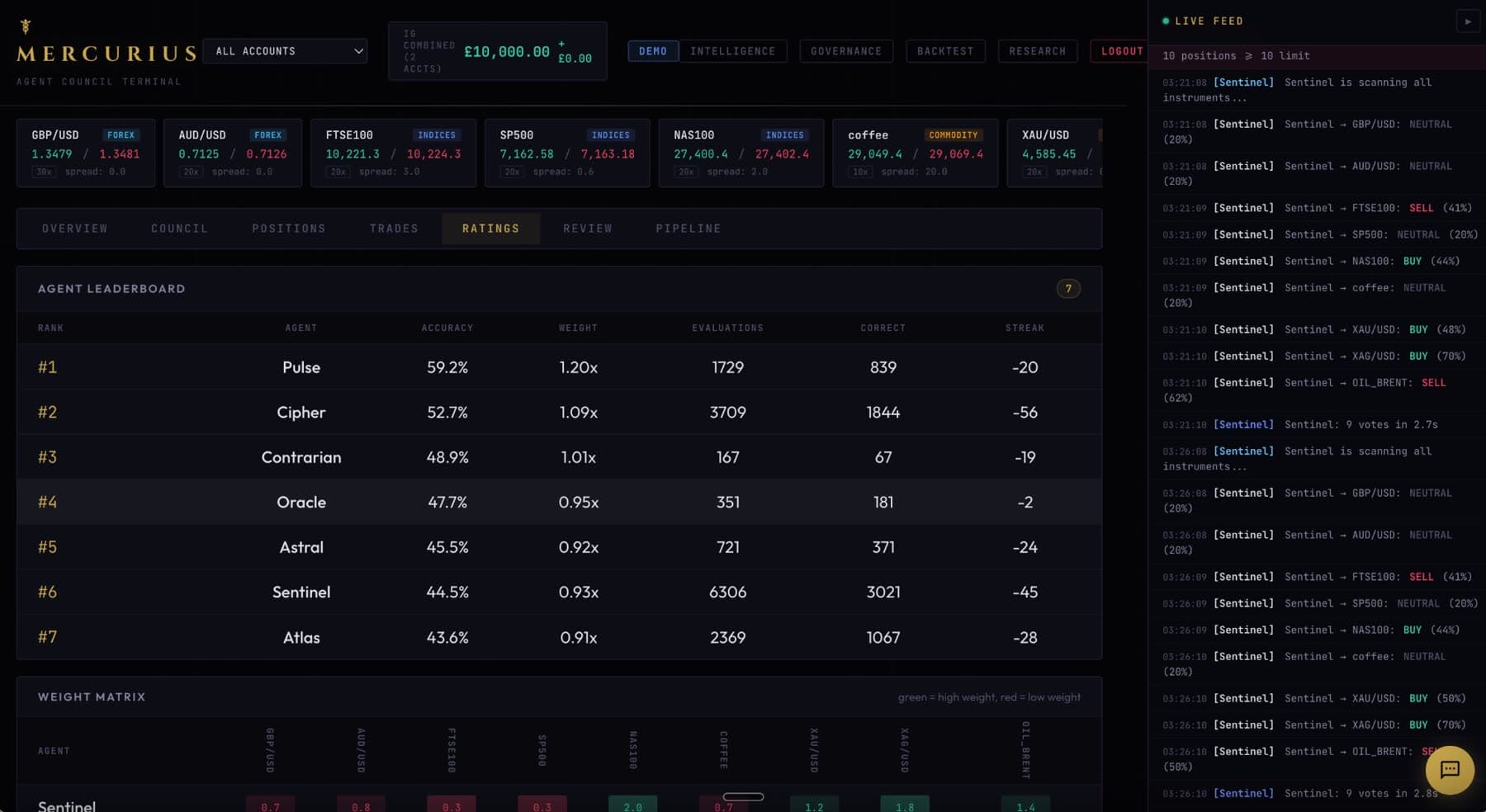

An autonomous trading system. Six agents, each reading a different slice of the market — Sentinel scanning, Atlas on macro, Cipher on technicals, Oracle on fundamentals, Pulse on sentiment, Structure on the tape. An Arbiter counting votes, consensus required before any position. A self-improving filter, a ten-layer guard system, three months live on a £100,000 virtual book, running around the clock. Built alone.

It never made money, and for a long time the answer was to add — more agents, more data, more machinery around the same signals. The harder move was to stop adding and start measuring. The system’s own database delivered the verdict: 1,325 closed positions, a total P&L indistinguishable from zero, no agent beating a coin flip at scale. The signals were noise. A council of agents all reading the same public data cannot manufacture information none of them has.

So I rebuilt it from the ground up around one rule: nothing trades without a walk-forward backtest that survives realistic costs. Then I tested the five best strategies available to a retail account with genuine rigour — cross-asset momentum, an event strategy on coffee, FX carry, futures positioning, vol-targeted momentum. Every one came back a loss after costs. And where real signal existed — twice, it did — the broker’s overnight funding charge erased it. That drag scales with position size. You cannot trade smaller to escape it.

So I wound it down — not because it broke, but because it was proven. A negative result you can trust is worth more than a positive one you can’t.

The apparatus outlived the experiment. The backtest engine, the honest cost model, the pre-committed stopping rule — the method of measuring honestly and killing what doesn’t survive evidence — is the part I kept.